Intercompany transactions require significant attention and have always been a critical part of the financial analysis world in SAP. Certainly, this process is very complex, and it will require significant resources with different levels of expertise as operational reporting and business requirements become more detailed.

In this article, we will learn the latest updates on the topic that have multiple names such as Profit in Inventory (PII), Intercompany Profit Elimination (IPE), Transfer Pricing and many more names. The purpose of this article is to provide light, not fully answer or resolve your problems for this you can call

Arellius Enterprises to evaluate your specific requirements.

Solutions

For a start, let’s try to find a solution for this simple statement:

“Company A, located in Europe, has an order from a customer in Europe. However, in order to fulfill the order of 1,000 units of one product, the company needs to source different plants/companies located in USA, South America, Europe, and Asia. At first, Company A knows it has 500 units available in its inventory to provide to the customer ready to go in Europe. Yet it will need the other 500 units from somewhere at the minimum cost possible for them and to maximize Company A profit. Right now, Company A sees in the system the inventory locations worldwide of this ONE Product in warehouses around the world such as: 200 units in USA plants/companies, 250 units in Asia plants/companies and 50 units in South America plants/companies. In addition, you must negotiate with those plants/companies independently since they also sell that product to their customers, and they have different product margins, safety stock criteria and you are just another customer to them. Remember, again it is just one product and if needed expand the same logic if you had 100 finished products in one order for this customer.”

Notice that I put the name “plants/companies” since the analysis could be done at the company level or to a plant that belongs to a company in your organization, or the plant belongs to a supplier. In order to have enough inventory to provide to the customer, there are many scenarios for Company A, such as:

- Provide the customer with all 500 units available and place the others in backorder until you find the other products and arrive at the customer location directly while they are produced from other corporate plants/companies.

- Commit with the customer to deliver the 1000 units on a future date, considering that all plants must ship the units to the warehouse(s) in Europe, thus different shipping costs from the different locations to the customer directly or to Company A warehouses then to the customer. In addition, this scenario requires analysis to evaluate if it is cheaper to ship directly or to your central warehouse in Europe while keep fingers crossed if your cargo won’t be delayed due to the War in Ukraine or taken by Pirates around the Gulf of Aden or “confiscated” by another foreign government since it did not like the latest sanctions against them or they found illegal drugs in the shipment so the cargo wont be released until the court in that country finishes the investigation, and you are back to square one and need to find other supply somewhere else.

- You can source third party suppliers and provide all your 500 units in your Europe warehouse now to the customer and the others to be manufactured or shipped to the customer from suppliers using Company A packaging and ship it directly to the customer or to Company A warehouses and from there to the customer. The customer will accept the delay with a discount only otherwise it will go to the competition.

- Provide 400 units to the customer while keeping 100 units in safety stock for other customers that you don’t want to lose for future sales, and you have something to give them for a while and combine the sourcing from suppliers and internal plants/companies with a multiple profit margins per shipments and taxes per jurisdictions. If your suppliers/plants are in India or Brazil, you are about to open another Pandora’s box, since they are the two most difficult tax jurisdictions in the world.

- You provide all your 500 units and buy from the other plants/companies in USA, South America, and Asia a mix of product some semifinished and other finished goods. You can produce the goods with your suppliers or your own plants; while having limited access to finished goods because the other plants/companies also have safety stock levels that they must keep for their regular customers, and you are not one of them.

- Your Big Four consulting company brings you a proof of concept (POC) with the coolest cloud solution to interface with SAP and another consulting firm says that this product is obsolete, and SAP does not support it any longer. After all is almost set and done, the Financial Consolidation team must double check that your data is not entered twice for the intercompany transactions and profit in inventory has been eliminated in Group Currency. Then your Big Four Consulting firm will meet another consultant that will say that Product field you need to run your report does not exist in the current SAP Consolidation scenarios, and your SAP S/4HANA installation is too old, and you need to upgrade to see the Product Field and being able to use it in Consolidations. Now, you have the Director of IT involved, and they will be asking for money to upgrade, and your team now is part of the testing of this solution, and now emergency budget needs to be approved… congrats!

Now that we see that this is a supply chain problem, Integrated Business Planning (IBP) consultants will say, hey we can do this, no problem but the data volume might be an issue you must reduce your data volume! Corporate Finance consultants will say this is operational we have no interest to know nothing at the product level, Operational Finance will say certainly it is critical since the we cannot guarantee the goal success of each individual company when we have intercompany sales, so we don’t know the real profit of our product mix per plant/company.

Tax accounting will jump in and say we need the taxes calculated in each sale across plants/companies must be removed besides the transaction elimination. You Big Four consulting and auditing firms will jump in to provide you solutions without telling they never done it, or they outsourced the job to another company you never heard. Guess what, all this simple but sophisticated scenarios must be taken all together at once and NOT from a planning point of view since Actuals will have all these scenarios and more.

Yes, they are all possible at the same time unfortunately, and yes, I have been there in all these situations.

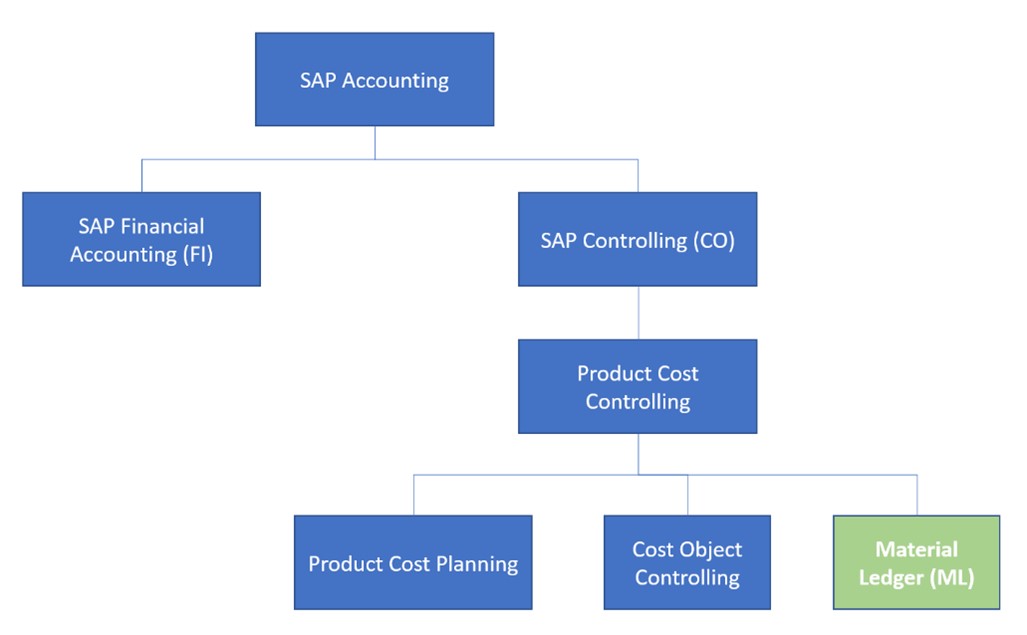

SAP Material Ledger (ML): General Overview

For many years now, SAP Material Ledger (ML) existed as another ledger. Due to the issues identified in the previous section it has become more and more relevant for multinational firms. ML is an SAP Ledger such as AR, AP, Assets, and interfaces with MM, PP, and SD modules as well as shown in Figure 1, and it is part of the Product Cost Controlling module. ML provides greater level of detail to analysis Raw Materials, Semifinished Goods, Trading Goods (purchased for resale purposes only), and Finished Goods. A general comment that becomes confusing is that for ML the term PRICE is equal to COST of the product, not the selling price but the module is configured to see Price as a term.

Just as reference, if there is

no intercompany markup when inventory is sold or transferred from one plant/company to another one within the same corporation, the issue of Valuation, Profit in Inventory (PII), Transfer Pricing, Intercompany Profit Elimination (IPE), or any other name,

it will not be relevant. However, if there are formal intercompany sales or inventory transfers with Price Markup then this process is relevant for your organization and ML comes to the rescue.

Also, when you hear the term Inventory valuation it is just the process to establish the cost of the materials owned by a plant/company. Standard Costing or Moving Average methods are used to manage the inventory valuation as materials fluctuate over time in order to quantify the true value of your inventory. For example, every time an invoice or goods receipt occurs the moving average is updated.

In ML when you hear PRICE, like “prices are rising…” it means COST in the system, which creates confusion when from a sales perspective. Price Markup in summary can be defined as the intercompany markup is increased selling price from sender to receiver plant/company. For example, when Company 1 sells to Company 2 with 10% price increase, and Company 2 sells to the customer.

When there are multiple prices or discounts/promotions when sold from one company to another, the issue that a company within the same group must eliminate any intercompany profit as part of their reporting since we are all the same company we just used the inventory from one company to sell it to a client from another company within the same corporation. However, industries such as Pharmaceutical, Chemical, Metallurgy, Oil & Gas, Healthcare, Manufacturing, Logistics, Retail and others; monitor margins at the product level and the concept of Group Valuation is relevant from an operational, business or legal requirement to either use ML Actual Costing or Parallel Valuation to have a parallel cost of goods manufactured (COGM), inventory valuation, and cost of goods sold (COGS).

Figure 1— Material Ledger as a Subledger of the SAP Controlling Module

Figure 1— Material Ledger as a Subledger of the SAP Controlling Module

In general, it is possible to simplify the benefits of ML as follows:

- Ability to valuate inventory based on Actual cost.

- Easy identification of intercompany profit in inventory.

- It is possible to visualize material COSTS in multiple currencies, WITHOUT Currency Translation Adjustment (CTA). However, if you want CTA another enhancement and customization, if you are using it in SAP BPC/SAP Group Reporting then discrepancies might occur, so I highly recommend do not implement this customization in ML.

- Greater detail of the material activities within the period.

- Ability to manage transfer pricing between profit centers.

- Determine the true cost of sales by transferring variances for unsold stock inventory.

- Allows measuring profitability and estimate a more accurate inventory valuation using Legal (generally Local Currency), Group (generally Group Currency, and allows to exclude the Price Markup), and Profit Center valuation (either Local or Group but posts to different fields in ACDOCA). You need to set up a structure in T-code 8KEM.

- Taxes are not part of the ML generally, if required it must be performed an enhancement of the additional levels of detail, but this is not relevant since ML is directly focused on Inventory Valuation without Tax, but it is possible to perform it with customizations.

- ML allows to post all valuation types (Legal, Group, and Profit Center) in the SAME Ledger or use multiple ledgers to implement each valuation approach. Please follow these OSS Notes 2882025, 2160974 and 3334743 to make your decisions what is best for your organization.

As you become more acquainted with ML, you will hear the topics Legal Valuation, Group Valuation, and Profit Center Valuation. They are summarized as follows:

- Legal Valuation: this is the default approach. A company code that is used in SAP records all transactions in the Legal View to be compatible with the rules of the country that the company resides in. Here aligns with Company Code Currency fields.

- Group Valuation: this approach is used where an organization is made up of multiple entities that transact with each other and want a group view of inventory costs that eliminated any intercompany profit due to markup. Aligns with Group Currency fields, and no Currency Translation Adjustment (CTA) is performed. To be clear this is NOT SAP Financial Consolidation and Elimination, it is just focused on Inventory valuation. In simple terms, if you sell the same product to yourself, you are not making money, thus the inventory value is the same across the supply chain if within the same Group.

- Profit Center Valuation: this approach is used where a company contains subentities that are represented by profit centers and want to record any profit that occurred from transactions between these subentities. Uses separate fields in ACDOCA table.

Figure 2— Example of ML Legal vs Group Valuation Scenarios for the same Group for ONE Product Price (Cost).

Figure 2— Example of ML Legal vs Group Valuation Scenarios for the same Group for ONE Product Price (Cost).

SAP S/4HANA Group Reporting: General Overview

After a long great history using SAP BPC (Business Planning and Consolidation), SAP released the SAP Group Reporting tool as the new consolidation tool within the SAP S/4HANA landscape.

Just to be clear, SAP Group Reporting was released in SAP S/4HANA Cloud on May 2017 and September 2018, for SAP S/4HANA 1809 On-Premise edition. So, if you have team members saying they have 14 years of experience working in SAP Group Reporting, now you know something is not right in your team. If you have any doubts on this,

check this link on the official announcement by Christoph Ernst, SAP global finance solution management.

The latest version when the moment this article was written is SAP S/4HANA 2022, and to go into more detail it is recommended

to review this article from yours truly.

Figure 3 provides a summary of the architecture of the tool. As you can see the SAP Group Reporting Consolidation application is used to integrate planning data coming from SAP SAC (Analytics Cloud) and two other tools SAP Group Reporting Data Collection (to manage non-SAP sources) and SAP Disclosure Management (an electronic submission tool). Another tool also that SAP Group Reporting interfaces is called ICMR (Intercompany Matching and Reconciliation) and specifically designed to identify imbalances for intercompany transactions, like ML in certain ways but not with the same level of detail and focused on finance and consolidation intercompany imbalances, and analysis to the product level was not in its original purpose.

Figure 3— SAP S/4HANA Architecture Source: SAP

Figure 3— SAP S/4HANA Architecture Source: SAP

As from SAP S/4HANA Release 2021, SAP enhanced SAP Group Reporting and ACDOCU table to allow many custom fields to be added. Significant changes occurred with the release of SAP HANA 2022 regarding extensibility:

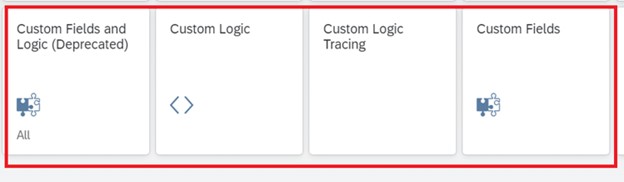

- The previous Fiori Tile called “Custom Fields and Logic” has been deprecated, meaning DO NOT USE if you are running SAP S/4HANA 2022 or higher. The previous app has been replaced with TWO new apps called “Custom Logic” and “Custom Fields” as shown in Figure 4.

Figure 4— NEW SAP S/4HANA 2022 Apps for Extensibility

Figure 4— NEW SAP S/4HANA 2022 Apps for Extensibility

- These NEW Apps are available in the “SAP Application Services: Fiori Apps” catalog and they must be added to your security role in SAP S/4HANA 2022 with the catalog SAP_BASIS_TCR_T

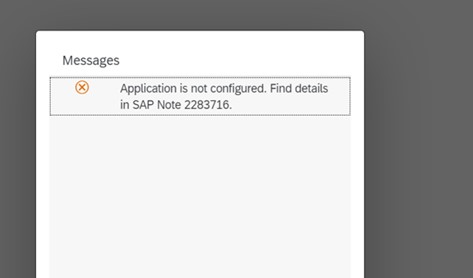

- On top of this, you must follow the configuration OSS Note 2283716 for the new Apps to run in your SAP S/4HANA 2022 environment, otherwise you will see the message shown in Figure 5, and your Apps will not launch.

Figure 5— Message displayed when you are missing configuration of your Extensibility Apps

Figure 5— Message displayed when you are missing configuration of your Extensibility Apps

Now from Profit in Inventory (PII), Intercompany Inventory Profit (IIP), Transfer Pricing (TP), Intercompany Profit Elimination (IPE) or any name you like to call the inventory markup eliminations. SAP introduced a program specifically created to manage these eliminations on SAP S/4HANA 2021. This means, yes you can perform the markup eliminations in SAP Group Reporting in the ACDOCU table as well without the need of Material Ledger! The new program is shown in Figure 6, and further information can be

reviewed in this article.

Figure 6— Method S2015 for Intercompany Elimination of Inventory Profit in SAP S/4HANA 2022/2021

Figure 6— Method S2015 for Intercompany Elimination of Inventory Profit in SAP S/4HANA 2022/2021

Challenges when using ML and SAP Group Reporting combined

Certainly, the last two topics of discussion will need to be evaluated by a significant larger group in your organization Finance, Operations, Tax, Supply Chain, and of course your Big Four awesome consultants. However, with the latest SAP S/4HANA 2022 improvements also bring multiple challenges, and some of the ones discussed below are just the start:

- Now that we can do this in SAP Group Reporting and ML, which one is the best? The tricky answer always it depends. If you have extensive knowledge of ML in your organization and your operations team likes it, then do it in ML. However, if you do not have ML certainly SAP Group Reporting can perform the operation however not at the same level of detail as ML since the ACDOCU table is designed for aggregated data and might not have all the detail you expect from an operational point of view.

- Will the ACDOCU be able to manage the high data volume linked to Profit in Inventory elimination due to the Material (Product) level of information? Another tricky question, since It is so new it is still early stages, however, ACDOCU can be partitioned to accommodate unlimited amount data in this table following standard SAP system optimization procedures. The same will be true if ACDOCA will have data volume issues with ML.

- Is ML a consolidated view of my operational data? NO, ML is just focused for costing purposes for COGS or COGM, and certainly the ONLY tool available in SAP landscape currently for consolidation is SAP Group Reporting. On top of this, the consolidation process requires in a multicurrency environment to perform Currency Translation Adjustments (CTA) and the ONLY tool in the SAP Landscape capable of performing this task is SAP S/4HANA Group Reporting. ML is an operational tool that can handle multiple currencies, but no CTA calculations are possible with this tool unless you spend a significant amount of customization effort for something that will NOT be useful from a consolidation point of view since you will have to run CTA again in your consolidation tool or get ready to perform CTA Adjustment Journal Entries, which are mega fun to calculate. Just imagine you are a warehouse manager, CTA calculations will provide zero value for your day-to-day analysis, however, the overall cost for the Group Valuation certainly will help you to measure your profitability and operational goals.

- If we implemented ML and SAP Group Reporting, and if we are using Group Valuation in ACDOCA table which would be the source of my consolidation data? Another interesting question depends on many variables my recommendation following standard SAP design would be load Local Currency, which is aligned with Legal Valuation, and perform all your consolidation activities using that information. Use the Group Currency in alignment with Group Valuation for your granular analysis of your product costing scenarios, and do not confuse the purpose of the two. The most important recommendation would be made sure that when the data is loaded double check you are not loading the data twice which is another common error when implementing both SAP Group Reporting and ML.

- What about Cash Flow? A very challenging question, I recommend evaluating these two articles on creating a real-time cash flow report and generating your cash flow report automatically, and adjusting to your needs.

Conclusion

In this document I did my best to provide you guidance and concepts related to the topic of Profit in Inventory Elimination or markup elimination, transfer pricing and among other names. It is a very complex problem and might require very sophisticated solutions depending on the realities of your industry. However, the key part is that you clearly spell out your reports, the type of data that you want to see and certainly the level of detail that you would like to have for your technical teams to help you to make appropriate decisions. As mentioned, tax is a very complex topic and expectation for example to reverse the taxes calculated in the Group Valuation view as well not only the markup require further analysis considering the topic also opens a Pandora box in many countries. I hope this document has provided some light of the new functionalities available in SAP HANA 2022 product, and the new tools available to you to deliver your analysis, and as always it is recommended do not overdo it since this can also cause significant performance issues in your near future.