Value Chain

Michael Porter, Harvard Business School professor and one of the world’s most influential thinkers on management and modern strategy, defines strategy as “how an organization faced with competition achieves superior performance.” According to Porter, organizations must look beyond just efficiencies and effectiveness improvements to keep ahead of their competition. A competitive advantage is achieved when an organization’s profitability is sustainably higher than its rivals—either by leveraging premium pricing, lowering costs, or a combination of both.

To help organizations understand their competitive advantage, Porter developed a powerful framework called value chain analysis (

VCA) that organizations worldwide have used for decades. The VCA allows organizations to identify and focus on activities that result in higher customer value and price or lower costs.

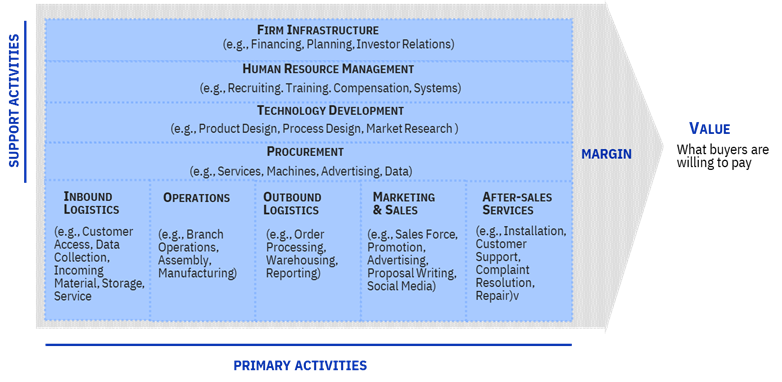

To illustrate, Figure 1 shows Porter’s value chain framework, where he divides the activities into two groups: primary and support. Primary activities directly relate to the final product or service (i.e., logistics, operations, and sales). Support activities help the primary activities such as procurement, finance, and human resources become more efficient. Both groups impact an organization’s margin performance and the value a customer is willing to pay for a product or service.

Figure 1- Michael Porter’s Value Chain (Source:

Harvard Business School in Boston, Institute for Strategy and Competitiveness)

Competitive Advantage

Organizations must master each activity as a step that adds value to the finished product or service to achieve a competitive advantage. They need to know their activities, the interconnection between them, which ones add the most significant value to their customers, and how these activities affect overall profitability.

When facing the speed and complexity of current business scenarios and their value chains, it is easy to see how organizations find it challenging to execute a complete and systematic VCA.

Consider your SAP system and how it was designed. Which activities were in place at the “conceptual” design, and how has your organization outgrown those activities? Can your SAP applications provide the necessary information to support your organization’s end-to-end value chain analysis, competitive advantage, and strategy?

For SAP ERP long-term customers, successfully managing value chains typically requires significant effort to reduce inconsistencies and inaccurate information. The good news is that innovative technologies in

S/4HANA are going in the right direction to support integrated end-to-end business processes and visibility to activities within the value chain. Many functionalities are already available in SAP S/4HANA to improve the view of the value chain in real time and consistently across all levels of an organization.

S/4HANA

An example of S/4HANA innovation in this area is the Display Material Value Chain

Fiori App, which shows the progression of material quantities and values along a product value chain (see Figure 2). The app shows the flow of the valuated material transactions from procurement, intracompany and intercompany transfers, production, and sales. Color-coded nodes display material value records, and the connectors between the nodes show the valuated transactions.

Figure 2- Display Material Value Chain (Source: SAP Fiori Apps Reference Library)

As another step to support the end-to-end VCA, SAP released in S/4HANA Cloud 2105 a business function called Universal Parallel Accounting (UPA). This function became available at the end of 2022 to

S/4HANA private cloud and on-premise customers. UPA came to fill the management accounting gaps, visioning to create the foundation to record the value in each chain step.

The UPA vision is to provide strategic business outcomes to organizations such as:

- Local and centralized VCA supporting different organization demands, including the support to identify competitive advantage opportunities.

- Visibility in logistics quantity and value flows from legal and group views, including inter/intra company sales and stock transfer, subcontracting, consignment, returns handling, etc.

- Harmonized architecture to approach multiple currencies and multiple valuations across asset accounting, production accounting, inventory valuation, and margin analysis.

- Foundation for value chain intelligence that recognizes and learns from business patterns.

Currently, S/4HANA is delivering the VCA foundation and enriching use cases like intercompany and valuation based on multiple accounting principles. The SAP plan is to deliver new business cases and models using value chain data and context, such as process mining, to find value chain inefficiencies and add nonfinancial measures to the value chains like Transactional Carbon Accounting.

Now that we have examined the importance of VCA and S/4HANA UPA vision, let’s review some current S/4HANA use cases.

-

Multicurrency Capabilities

With S/4HANA and Universal Journal, customers can use up to 10 parallel currencies. However, the controlling processes still use only two currencies (object and controlling area currencies). Material Ledger traces a maximum of three material ledger currencies, and asset accounting is tied to the three FI integrated currencies. The difference in currencies results in conversions at the posting, often leading to undesired currency effects in secondary processes such as depreciation or settlement.

UPA simultaneously supports the same currencies across all processes in FI-GL, FI-AA, CO, and CO-PC-ML application components.

-

Parallel Valuations for Unconsolidated Views

This use case means consistent calculations and posting values for all required accounting principles (e.g., IFRS, Group GAAP, and Local GAAP). A classic version of the parallel or multiple valuations’ function has existed since SAP ECC, but it is inconsistent across all modules. For example, in controlling, during distribution, assessment, and settlement, instead of flowing parallel postings for each accounting principle, values in the leading ledger are copied to all accounting principles.

SAP delivered a solution in ECC Ehp5 to solve the requirement for multiple accounting principles valuation of inventory. It is based on the business function “parallel cost of goods manufactured” (FIN_CO_COGM). The solution uses the classical multiple-valuations ledger with a parallel actual version of the activity types’ rates and material ledger/alternative run to calculate a parallel actual costing and use it for margin analysis.

The UPA solution covers the requirement for end-to-end multiple accounting principles valuation by using single-valuation ledgers to separate valuation views. By using UPA, you carry multiple accounting principles across the entire value chain, from primary costs to allocations, inventory valuations, and margin analysis. The same material with UPA can have multiple prices, standard costs, and thus production variances and contribution margins in each ledger, providing an end-to-end view of product profitability based on accounting principles.

-

Parallel Valuations for Consolidated Views / Group Valuation

This may be the most expected and impactful innovation to the value chain analysis. It focuses on achieving a group view for intercompany value flows distinct from the transfer prices used by the legal view, allowing organizations to capture group margins and Cost of Goods Sold (COGS) at the group level at each process step.

You may already be familiar with the group valuation approach with SAP ECC. In ECC EhP5, SAP released the business function “Stock in Transit and Actual Costing” (LOG_MM_SIT), which supports an organization’s cross-company code stock transfer with valuated stocks in transit and actual costing cross-company codes. The material ledger/actual costing then includes stock in transit in the actual costing multilevel price calculation.

UPA takes the group valuation to another level by introducing a consolidation-like approach that uses a separate single-valuation ledger specific for group valuation to eliminate intercompany revenues and COGS. With UPA, the intercompany goods movements are recorded “at cost” across the value chain, ensuring that profit in inventory is excluded in the group view.

Now that we have seen three UPA use cases directly affecting VCA, let’s review its deployment options. The UPA features are achieved by activating the business function FINS_PARALLEL_ACCOUNTING_BF. This business function also builds the foundation for future innovations in asset, inventory, overheard, production accounting, and sales accounting.

FINS_PARALLEL_ACCOUNTING_BF is automatically activated in S/4HANA cloud deployment. For private cloud and on-premise deployments, this function has been optional since the end of 2022. It is important to note that activating this business function needs to be carefully studied. There is a series of prerequisites, current limitations, and profound implications in multiple business processes of S/4HANA, which I will detail in future articles. In addition, once this business function has been activated, it cannot be deactivated.

Summary

In summary, SAP S/4HANA UPA harmonization and vision give customers great visibility into all activities and their respective values, allowing organizations to understand the entire value chain and find opportunities for competitive advantage.

Be on the lookout for a follow-up article presenting how Universal Parallel Accounting and Advanced Intercompany Sales replace the “classic intercompany process,” given a fully documented value chain and real-time view of group profitability.

For more information, you may contact the author at vanda.reis@ibm.com.