Google Discontinuing Cloud IoT Core

In case you missed this big update, Google Cloud Platform (GCP) users using the Cloud IoT Core product offering reported receiving a communication that it has added IoT Core to the end-of-life list and will discontinue in a year. This is a significant announcement, specifically for Industry 4.0 enthusiasts. In SAPinsider's research

Modernizing Logistics and Inventory Tracking, we discussed the role IoT will play in helping organizations build true end-to-end visibility. Embedding IoT in their technology infrastructure is necessary for most supply chains that look at true, end-to-end, real-time supply chain visibility. This end-to-end, real-time visibility requirement emerged as one of the top drivers in our most recent supply chain report,

Supply Chain Planning in The Cloud.

As per

IT News, the exact communication announcing this decision states: “We’re writing to let you know Google Cloud’s IoT Core Service will discontinue on August 16, 2023, at which point your access to the IoT Core Device Manager APIs will no longer be available. As of that date, devices cannot connect to the Google Cloud IoT Core MQTT and HTTP bridges, and existing connections will shut down."

What is Google Cloud IoT Core, and What is its Relevance to Industry 4.0?

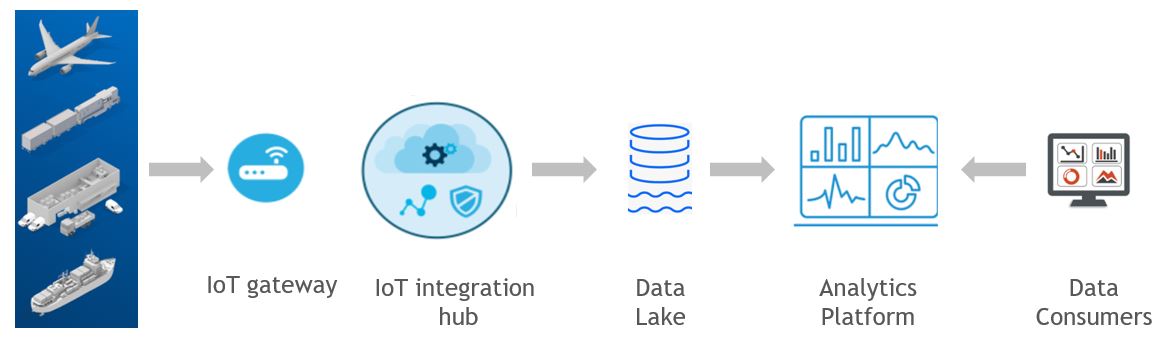

Let us start with the official description, as GCP puts it: "IoT Core is a fully managed service that allows you to easily and securely connect, manage, and ingest data from millions of globally dispersed devices. IoT Core, in combination with other services on Google Cloud, provides a complete solution for collecting, processing, analyzing, and visualizing IoT data in real time to support improved operational efficiency." Beyond the description, the role of IoT devices will be significant in the world of operations and supply chains. Consider this example from the Google Cloud IoT Core webpage to understand why IoT is critical in the operations and supply chain.

Figure 1: Example architecture leveraging Google Cloud IoT Core

Source: https://cloud.google.com/iot-core/

On the far left side of Figure 1, you see many assets. From Mobile assets like tractors or trucks to remote assets like a drilling rig in the ocean, IoT devices capture and relay critical data. So, as mentioned above, for many organizations, real-time end-to-end visibility in their operations and supply chain is not attainable at all if they do not include IoT in their infrastructure. The other important aspect to note is that the only way to capture this data, in streaming format, in real-time, from these devices, most times, is through interconnectivity with infrastructure as a service (IaaS) offering. And this is where we get into the opportunity that hyper-scalers have in this arena. Figure 2 from Fortune Business Insights illustrates the Industry 4.0 market by 2029. As emphasized in many articles like this one, I think these projections are less than a genuine opportunity.

Figure 2: Industry 4.0 market share projection

Source: Fortune Business Insights

What Could Have Driven This Decision?

So clearly, there is an attractive Industry 4.0 market that Google may miss if it discontinues this product and does not replace it with another. So what could be the drivers behind Google's decision?

Before we jump into the hypothesis, I think it is important to understand my perspective on the key ingredients needed to dominate the cloud market. Please refer to this article,

The Three Ss of Dominating The Cloud Market, before reading further.

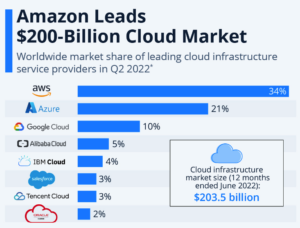

Now let us review these recent cloud market share numbers in Figure 3 before we jump into our hypothesis.

Figure 3: Cloud market share statistics

Source: Statista.com

An important point you need to keep in the back of your mind is that the chart above gives the percentage of shares of the total market. It is not showing the size of the market. Cloud business is booming, and I expect it to continue that course for at least a decade. So even if the percentage share for a player does not change significantly YoY, the Dollar revenue is certainly increasing, as you would observe from earnings announcements. But that is also a problem if your percentage share is relatively the same or has not grown significantly. It means that as the market expands, because of the cloud creating new opportunities, you are not being able to leverage those new opportunities to penetrate further into the market by creating new subcategories within the market and becoming the dominant player within those categories.

As mentioned in the article, what was once attractive, and still is from a cost perspective, the Infrastructure as a Service (IaaS) aspect has been commoditized at this point. That is why we see more and more PaaS solutions from the hyper-scalers to create differentiated products and services. The market is still booming because of demand, and as I consistently highlight, this demand will exist for at least the next ten years. However, the long-term success in this market belongs to those who "lock in" their customer beyond the infrastructure aspect. And the challenge in this, from a specialized solutions perspective, is that if you lag in any of the Ss highlighted in my article, the gap between you and your competitor will keep increasing significantly. AWS and Azure have made significant progress in the Industry 4.0 domain with their IoT platforms.

AWS IoT and

Azure IoT have amassed a massive pool of use cases. Since scale combined with solutions creates a speeding effect on the capability maturity, this massive pool has given them an edge, a very significant one, over GCP IoT. So the driving factors behind this decision are:

Lack of current state penetration: Offering a platform requires more than infrastructure. Many resources go into developing, maintaining, and enhancing such sophisticated offerings. And as with all business initiatives, it comes down to the return. Currently, the differentiating aspects of IoT platforms are few. Look at Figure 4 where we share simple architectures from the three hyper-scalers.

Figure 4: IoT platform architecture examples of three hyper-scalers

GCP

AWS

Azure

Azure

As you can see in Figure 4, other than the names of offering components being different in the architecture, the gist remains the same. The functionality of the IoT core or hub remains the same. So clearly, that is not where the differentiation is. I consistently emphasize that the differentiating aspects lie on the right, the AI and ML solutions that can be built using these platforms. Helping customers build unique solutions to leveraging these platforms is where the moola is, but that is not within this article. The gist here is that with the IoT platforms close to commoditization and maybe a lack of breakthrough solution creations with current use cases, the current state does not look very promising.

- Lack of pipeline: They may have also factored the development pipeline to enhance the solution, use case explorations with current and future state customers, and decided that the future state pipeline does not look attractive enough to keep investing to further build this capability. Based on the Three Ss, scale creates a massive edge, and the larger your customer base, the more experimentation opportunities you have. AWS and Azure enjoy that edge, meaning they can use that to keep increasing the gap.

- More important focus areas: Alphabet is in flux and transformation. It realizes that its core business needs to develop and transform. Its workforce, mindset, and culture need to develop as well. Recent hints on taking extreme measures to improve productivity and innovation are indicators of this as well. I can think of a few areas associated with their current strengths that they can foray into to create new categories entirely. So I am sure that much smarter folks at Google have already identified some key opportunity areas. The plan now is to focus on development and execution in those areas.

- Possible partnerships: Since the market is too attractive to be ignored or walked away from, I suspect that GCP may have partnered with specialized edge computing platform providers, like ClearBlade, that are offering a transition to GCP IoT Core customers.

- An enhanced replacement product. I feel they may have a more robust, innovative product in the pipeline, which they do not want to disclose yet, since it may still be in development. This also looks like a strong possibility since, at the cost of sounding like a broken record, the market is too lucrative just to walk away from it. Partnerships can help get you in this market but not the control you need to be a significant change.