4 minute read

Keeping pace with technology in financial management can be a tricky endeavor. Intelligent automation (IA) has caught the attention of finance professionals at enterprises large and small and is being adopted at impressive rates. But what exactly is IA? It is the breadth and complexities of mechanizations, such as robotic process automation (RPA) and artificial intelligence (AI), existing on a technology-spectrum defined as IA. While innovation buzzwords such as machine learning (ML) and trends like RPA abound, it’s helpful to slow down the bandwagon before jumping on it to understand exactly what these buzzwords and trends mean. In terms of financial technology considerations, it’s crucial to understand such differences. So, this is exactly what this blog is devoted to — where we will look at what RPA, ML, and AI truly mean.

Robotic process automation (RPA) essentially is advanced automation that mimics the process and steps taken by its human counterpart. It initially requires programming and guidance to accomplish steps, but once the programming is complete, the robotic component of the process can take over, thereby removing the need for manual processing or intervention.

RPA is adept for rudimentary and often highly repetitive process. It can execute more basic tasks without human intervention and is also referred to as “unattended RPA.” On the lower rung of the IA spectrum is “attended RPA” (or “desktop RPA”), which requires human assistance and works in tandem. The differences between the two are the following:

Explore related questions

Ask SAPi

- Attended RPA: Bots respond to employee-triggered actions by automatically completing certain tasks to simplify a workflow.

- Unattended RPA: Bots automatically complete back-office functions at scale with minimal employee intervention.[i]

Within finance, AR processing is an example of an operation that can benefit from RPA. For example, the data found in AR billing systems reflecting successful delivery of a product can then trigger an automated remittal of an invoice to the customer. There is no need for human intervention once the tasks and executable parameters are established. The repetitive process of sending invoices may be transitioned over to the RPA solution.

Machine learning (ML) has a much higher degree of algorithmic, computer-driven automation. Where RPA operates strictly within the parameters of its programming, ML has more freedom and ability to operate because its functions are greatly predicated on adaptive capabilities. These capabilities derive from its ability to learn and predict outcomes; hence the name “machine learning.” Learning via algorithm, in simple terms, translates to considering all inputs and variables and potential outcomes, as well as identifying (and avoiding) potentially problematic areas. Based on the anticipated best outcome, it then works to make this best outcome a reality. The greater the number of inputs and data, the more accurate or perceptive the outcome.

ML is being explored by internal audit and financial control teams. Those employees executing reviews often must interact with varying systems and teams to retrieve random samples/evidence of adherence to financial controls to satisfy auditing. This can be an intensely time-consuming and rather mundane process. However, when the audit review steps and procedure are programmed as inputs and variables to the ML algorithms, the outcome is the financial review and control process may now be automated. According to an article in CPA Journal: “Rather than relying primarily on representative sampling techniques, ML algorithms can provide firms with opportunities to review an entire population for anomalies.”[ii] As long as the initial inputs and algorithms, as well as the anticipated final outcomes, of course, are approved by the audit team, this task may effectively be taken out of human hands.

Artificial intelligence (AI) mimics human intelligence, while RPA mimics human actions — to put it clearly; AI is the culmination of robotic learning. ML is not unlike a precursor to AI in that it established the foundations and training on which AI operates. AI does not require additional information nor data from its existing, pre-trained foundation to learn. Rather it aggregates and analyzes historical data to make predictive and learned responses from previous operations devoid of human input or interjection. For ML to make a more advanced predictive response, it would still require additional inputs into its programming algorithm. AI makes its own inferences based on its machine-learned experiences. More so, AI can operate on a broader spectrum by incorporating tools such as generative adversarial networks to stress test and improve neural networks by having them learn from and test each other.

AI working in tandem with deep data creates a very attractive proposition. For example, AI can aggregate customer data and historical trends as well as use predictive analysis to anticipate future purchase and payment behavior. This capability supports multiple business functions and some of their tasks such as risk management in finance or upselling in marketing and sales. It’s no wonder that AI is given so much consideration at all business levels.

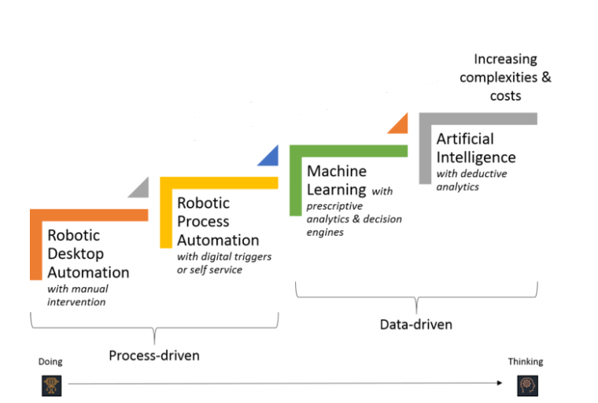

The figure below shows the transition just described — from attended RPA, which requires manual intervention, through RPA and ML, to complete data-driven AI with deductive analysis.

Source: Medium.com

Figure caption: As the automation increases in complexity – going from process-driven action to data-driven cognition – so too do the costs rise.

What Does This Mean for SAPinsiders?

- Embrace financial technology integration. The growing interconnectivity between process capabilities and data integration is almost boundless. Those organizations that recognize the benefits of adopting systems that can integrate enterprise-wide processes and particularly finance functions (such as SAP S/4HANA) and analysis (such as SAP Analytics Cloud) will ultimately prove to be more efficient and insightful. IA paves the way to this road.

- Maximize value-added tasks with your employees by automating mundane tasks. Process map and identify where RPA, ML, and AI can potentially execute tasks previously manually managed. Conversely, identify areas where increased employee attention will be well served, such as retention-based efforts, and transition resources accordingly.

- Identify relevant existing and anticipated benefits of IA in finance. As was briefly described, the benefits range from more process-oriented tasks, such as invoice management and payment remittal, to more complex functions, such as general-ledger management, to critically valuable tasks, such as risk management and predictive purchase behavior. The degree to which IA can assist largely depends on an organization’s willingness to invest in the technology and its level of commitment.

- Organizations should develop consistent technology reviews. It’s very likely that within six to twelve months’ time, this blog will be antiquated and obsolete, potentially missing the next advent of technology. That is simply due to the rapid pace at which technology advances. Don’t let this happen to your organization! To avoid having financial technologies experiencing similar obsoletion, schedule periodic reviews that formally address the operational, strategic, and technological goals with comprehensive assessments.

[ii] Gabe Dickey, Sandra Blanke, and Lloyd Seaton, CPA Journal “Machine Learning in Auditing” June 2019 www.cpajournal.com/2019/06/19/machine-learning-in-auditing/

More Resources

See All Related Content

UiPath IXP and the Case for Intelligent Document Processing in SAP EnvironmentsEnterprise teams are reassessing intelligent document processing as LLMs expand document interpretation. This analysis examines how UiPath IXP supports SAP workflows by improving data reliability, governance, and execution across finance processes.

How CCH Tagetik Defines and Scopes the Modern Financial CloseFinancial close is increasingly constrained by data alignment and reconciliation rather than consolidation logic. This article examines how CCH Tagetik Financial Close & Consolidation software addresses these challenges through unified data, workflow control, and automation, supported by real-world case studies.

3 minute read

How BlackLine’s AI-Driven Accounting Automation Is Reshaping the Operating Model for the Office of the CFOSAP CFOs face pressures to enhance finance operations, as 53% of organizations take four to seven days for financial closes, prompting a shift towards AI integration for faster, governed insights and automated processes, exemplified by BlackLine's architecture.

8 minute read

SimpleFi Links Better Dashboards With Finance Automation GainsSimpleFi Solutions says SAP finance teams should modernize dashboards and automation together, arguing that effective SAP Analytics Cloud and Business Data Cloud reporting requires disciplined, audience-focused dashboard design plus workflow automation that eliminates spreadsheet-based manual prep, reduces errors and keeps KPI data consistent for faster, more reliable decision-making.

3 minute read